“You have to ask yourself what amazing things come from just a little bid of greed. You show a path to cash and they will all come out of the wood work”. Friend of mine when I worked at Ericsson.

“Anyway, no drug, not even alcohol, causes the fundamental ills of society. If we’re looking for the source of our troubles, we shouldn’t test people for drugs, we should test them for stupidity, ignorance, greed and love of power.” P.J. O’Rourke

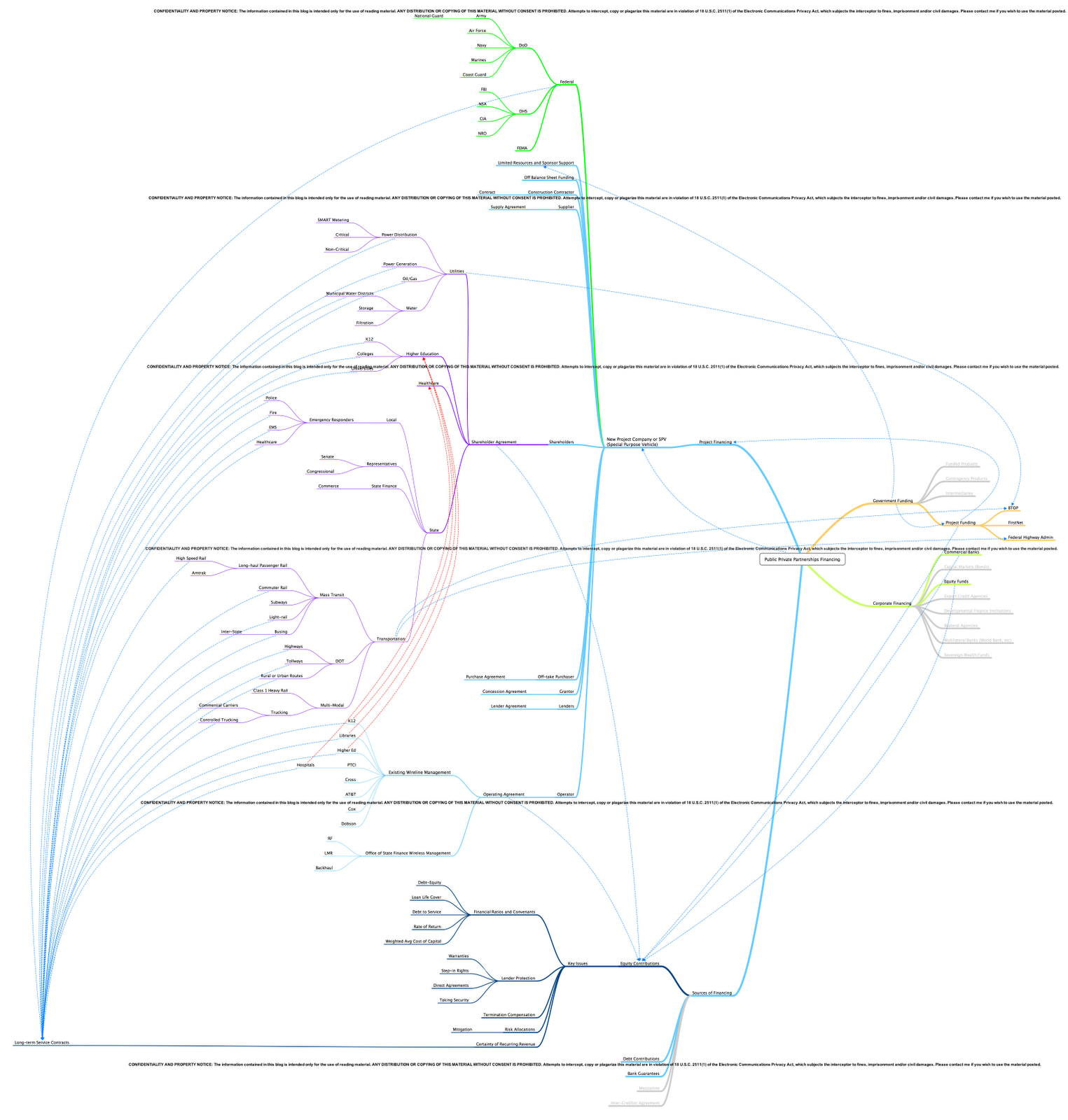

The complexities of Public Private Partnerships are unique tools of the trade. There has never been a sole telecommunications Public Private Partnership within the United State except for some small fiber builds back in the late 90’s. Even those were not very successful. Having spent the better part of 2003 until 2009 researching the topic of Public Private Partnerships, and their ability to help deliver the most complex telecommunication initiatives, they are tools that generate a lot of interest when it comes to cash. Although my dissertation topic back in 2009 was cased on the mass transit industry the idea is the same across all common verticals. The primary point is that there is a balance between business case aspirations; the need for technology to sustain operations; the best method of delivery; the reliance upon commercial technology roadmaps; and ultimately the course of “self-funding” programs and revenue generation that can be equally distributed among those that take part in the overall plan.

Balance Between Business Case Aspirations

If you work for a major Utility then try convincing the board of that Utility that it needs to be a telecommunication company. Even though it may sound like a reasonable opportunity to many that reside within the industry; I can assure you that the complexities of joining the “technology roadmap” are quite different and can put a major strain on both financial and human resources that go way beyond the original business aspirations of generating and delivering power. It is nothing new, and has been my experience, and the issue is always presented, to which many have succumb to the results; that being which business are we in…power or telecoms? The result is always the same. It doesn’t matter if you are in the Utility business, the mass transit business, the mineral and mining business or even the construction and infrastructure business… the result is always the same. Our primary business case is….

If someone out there can stand-up and demonstrate one successful major telecom job that has been successfully delivered within any other industry that has the revenue potential of what a carrier business model can deliver then please stand up. We need that business case to deliver to all the vertical industries.

The Need for Technology to Sustain Operations

I have helped design, build, maintain and operate telecom networks for more than 25 years now. I have worked on telecom solutions for high-pressure gas lines, oil gravity flow pipelines, well-heads, substations, RTUs, petro-chemical plants, major airports, mass transit solutions (to include subways, light-rail and heavy rail solutions), Class 1 Railroads, Highway ITS & tollways, healthcare, financial services, media & entertainment and even highly classified private networks; and oh yes…the telecom industry. That being 1st Generation, 2G, 3G and 4G platforms to include major fiber optic solutions for both backhaul, long-haul transport and metro fiber rings with multiple access scenarios. Across all the vertical industries the same technology is used. It may be called something different and distributed in varying manners, i.e. ITS, MANs, Broadband and/or transport networks, but in the end they all exist and operate on the same principles and commercial viability of the technology. The only thing that really matters is how it is applied to the business needs of those it is deployed for.

To illustrate: there are those within the Utility industry that believe a “telecommunications expert”, that “has never delivered a utility grid” has nothing to contribute to actual aspects of a power distribution network and thus has nothing to contribute to a Utility company. After all, taking an AMI interface modem that is wireless connected to a pole attachment, then delivered through a 3G cellular network and back hauled via microwave, or WiMax, and into a fiber optic point of presence so that it can be transported with SONET or DWDM transport platform ultimately communicating with a major network operations center and/or datacenter element really has nothing to do with power distribution itself anyway. Therefore I would suggest that maybe those people are right. The point being made is that the technology is the same in all the vertical industries. What is different is the business justification to making it happen and the foresight to build it correctly…the first time.

The Best Method of Delivery

In respects to the best method of delivery I am referring to the financial modeling tool that can help generate the capital needed to build, operate and maintain the telecom solution for the given industry client. This is where the financial delivery method becomes important. In my research I demonstrated that for a transit agency, or in this case a Utility provider, may NOT be best suited to design, build, operate and maintain a competing, and very complex, telecommunication business model within its owns operating model of the power business. Such a model competes for resources away from the primary object of that organization.

Another important point is that when Utility takes on its own telecommunications model, within its core business model, it buys into the fact that it must maintain the proper resources that must stay abreast of the latest and greatest in their given field; in this case telecom experts within a power utility company. I have personally witness levels of moral busting occur when young talented IT or telecom guys/gals are hired into a staunchly supported organization of power industry professionals. How do you explain the need to give a young 20 something year old engineer starting at 130k a year and then sit him in a cubicle next to a gentlemen that has been in the electrical industry for 40 years and is barely making 110k a year? I can guarantee that there will be some discourse. Simply the market paradyne does not mix in this case.

In short, let the Utility provider, transit Agency, or whomever concentrate on its core business to its clients and formulate a plan that allows the client to utilize a private network entity (not a commercial entity) to, not only build its communication requirements, but also take on the risk associated with the ever advancing telecommunication industry.

The Reliance Upon Commercial Technology Roadmaps

Risk. Its a short yet powerful word, especially when it comes to Public Private Partnerships. As was alluded to above; by taking on your own means to design, build and operate a complex telecommunications solutions, i.e. can’t get much more complex than the latest 4G LTE, you are exposing, not just your entire organization, but your entire business model and the survivability for the future. After all, who wants to spend $500 Million dollars on a new SMART Grid only to be informed a year before completion that the network is no good and you have to move to a brand new technology which will require a total rip and replace program. So how do you not get exposed to the risk? Well you let the risk ride with your P3 model.

A properly executed P3 model (that being Public Private Partnership) you will allow the risk to be carried by a centralized controlling agent, such as a newly generated private company — better known as a SPV or Special Purpose Vehicle. In short, as a Utility you have two options within a P3…you are a client that is getting access to the private bandwidth through long-term service level agreements and/or you have the option to be an investor in the network itself. Outside of the P3 model you can build it yourself, or use commercial services. With the lack of spectrum, and the complexity and costs associated with LTE broadband, to build it yourself will be unwise. Alternatively, to use commercial services you still do not relinquish the risk nor the cost impacts, of long term service availability, plus you may have issues with hardening requirements.

Ultimately the Course of “Self-Funding” Programs and Revenue Generation

For the sake of conversation we will focus on going with a P3. With a P3 you, the Utility, are a client to the Statewide Broadband Network in support of the National Broadband Public Safety Network. The State and the Federal Government become the tier one owners of the P3 model and thus have controlling stake in the venture and creation of a private entity that will design, build operate and maintain the private broadband network. This SPV, or newly created centralized State private entity, has the sole purpose of running a telecommunication broadband model for all the State entities. Those State entities would be Police, Fire, DHS, DOD, Agriculture, Forestry, Transportation and yes, Public Utilities (water, gas, power, etc..) to name a few. These make up the Public part of the Public Private Partnership. You may note that there is no competing business plans or overlap. The private centralized entity is purely there for the purpose of running the Statewide Broadband Network and in coordination with its higher element the FirstNet Board. The private entity will not do power, transportation or forestry services…only the broadband LTE.

In support of this model can be the availability of the State entities to also invest into the State P3 model. In essence, whether it is your existing assets, money or resource capability they can all be considered as a viable investment into the private centralized model for the State. Being that this is a “Public” and “Private” partnership, investor controls will always be maintained as proxies through the control of the State and Federal elements, or representatives, of the private centralized entities board, or shareholders. This State and Federal controlling element will never fall below 51% ownership of the P3 itself and thus the private centralized company setup to run the Statewide network. The remaining, or outstanding 49% ownership can be let to the private investments, i.e. GE Capital, Blackstone, or Warren Buffet, if they choose to invest. You should note that extra protection would be in place where as the newly created private venture would be backed by Federal and State resources; just in case the business goes under the State or Federal Government can take over.

As with any investment you need some type of return; in this case those returns will be generated through the long term SLAs, you as a Utility, will pay for to get access to the broadband network. That along with all the State entities (between 30-40 per state) would generate similar revenue through subsidized operational SLA agreements that let the risk to the private centralized state entity, or created company, that designs, builds, operates and maintains the network you need at the same time is responsible for maintaining its upgrade schedules. Those upgrades will be based on your requirements in your SLAs.

So there you have it. Quite simple if I may say so myself. Its quite clear to me on the outcome of where this is going. Of course others will truly believe that they can do better and achieve more than listening to some guy on a blog. 😉

CONFIDENTIALITY AND PROPERTY NOTICE: The information contained in this electronic transmission is intended only for the use of the individual or entity named above as reading material. ANY DISTRIBUTION OR COPYING OF THIS MATERIAL WITHOUT CONSENT IS PROHIBITED. Attempts to intercept, copy or plagarize this material are in violation of 18 U.S.C. 2511(1) of the Electronic Communications Privacy Act, which subjects the interceptor to fines, imprisonment and/or civil damages. PLease contact me if you wish to use the material posted.